Blind Tasting & Data Hub: what happens when labels disappear

There’s a particular kind of honesty that shows up in a blind tasting. People stop “recognising” and start reacting. They focus on texture, energy, balance, the way a wine holds your attention after the first sip. And suddenly you get a glimpse of what the market looks like when the usual signals like brand, price and reputation, step out of the way.

That was the point of the Wines Experience London Blind Tasting: to put Italian native grape varieties in front of an international audience, completely blind, and see what genuinely resonates. The Data Hub exists to capture those reactions and make them readable as insight that producers and buyers can actually use.

A note on the line-up: the selection wasn’t proportionally balanced, and Sardinia represented the majority of the wines. That happened because participation was voluntary and free for wineries, meaning some regions chose to enter more wines than others, and Sardinian producers were particularly active.

So yes, this naturally gives Sardinia more visibility in the results. At the same time, the patterns that emerge are still useful, because the tasting reveals how people respond to styles and identities when they’re not guided by labels.

The tasting was read through four analytical lenses: Most Liked Regions (MLR), Most Liked Grapes (MLG), Perceived Value per Price (PVP), and Top Ranked Wines (TRW), with each category also broken down by wine type (red, white, sparkling). Put together, these lenses tell a simple story: the audience responded strongly to wines that combine character with clarity, wines that feel distinctive without feeling heavy.

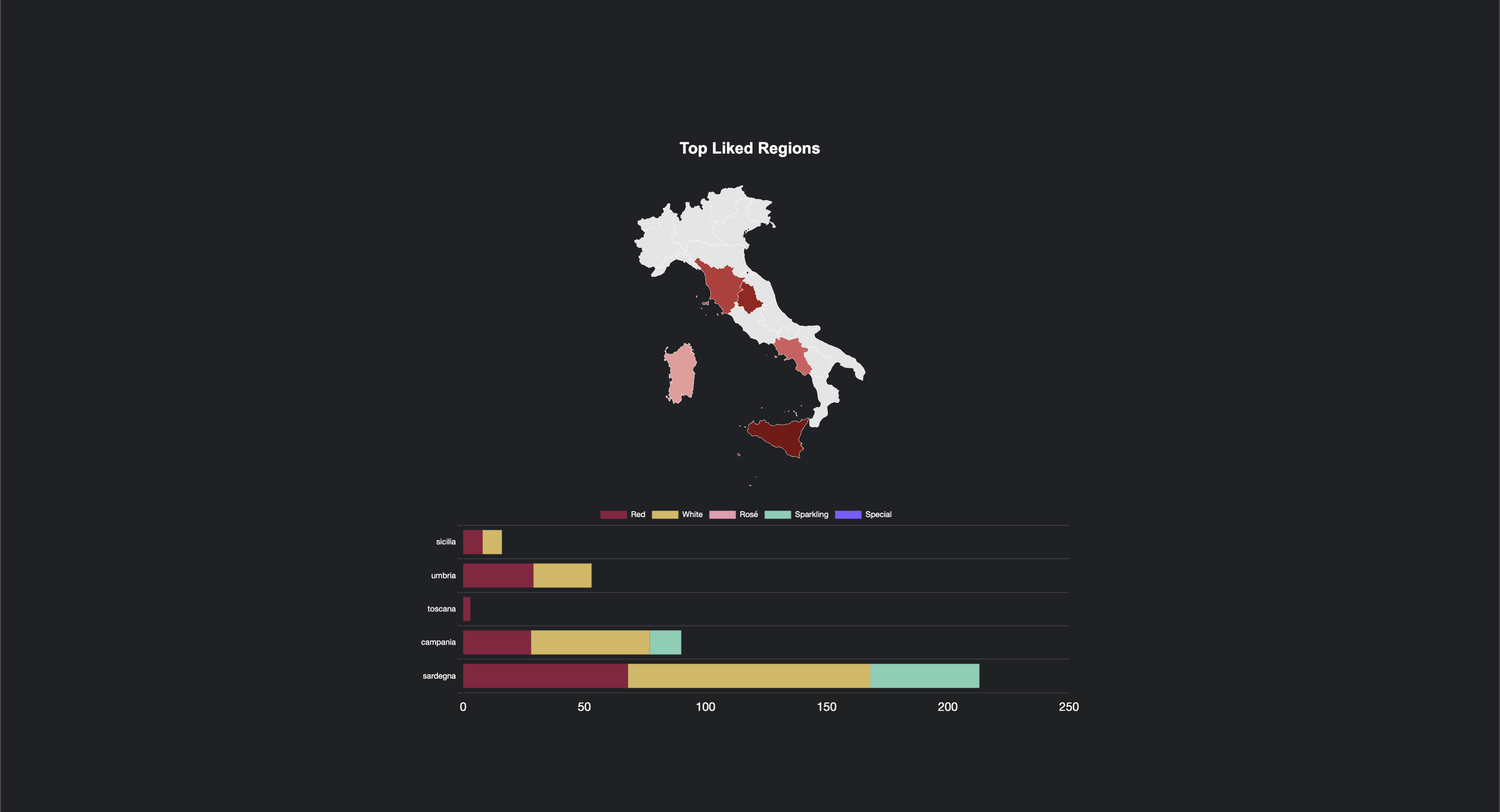

Most Liked Regions

Even taking representation into account, three regions consistently surfaced at the top: Sardegna, Campania, and Umbria. Sardinia dominated by volume, but it also held strong average enjoyment scores, which suggests it wasn’t winning purely because it was present more often.

Two other signals matter:

Sicily performed especially well in whites, taking the top regional spot there with an average enjoyment of 5.50 out of 7 despite fewer wines in the line-up. That points to a London audience that’s open to whites with strong terroir identity and tension.

Emilia-Romagna showed meaningful presence in sparkling, alongside Sardinia, which is consistent with how the sparkling category often succeeds: it’s easy to understand, easy to pour, and tends to create quick “yes” reactions at a tasting table.

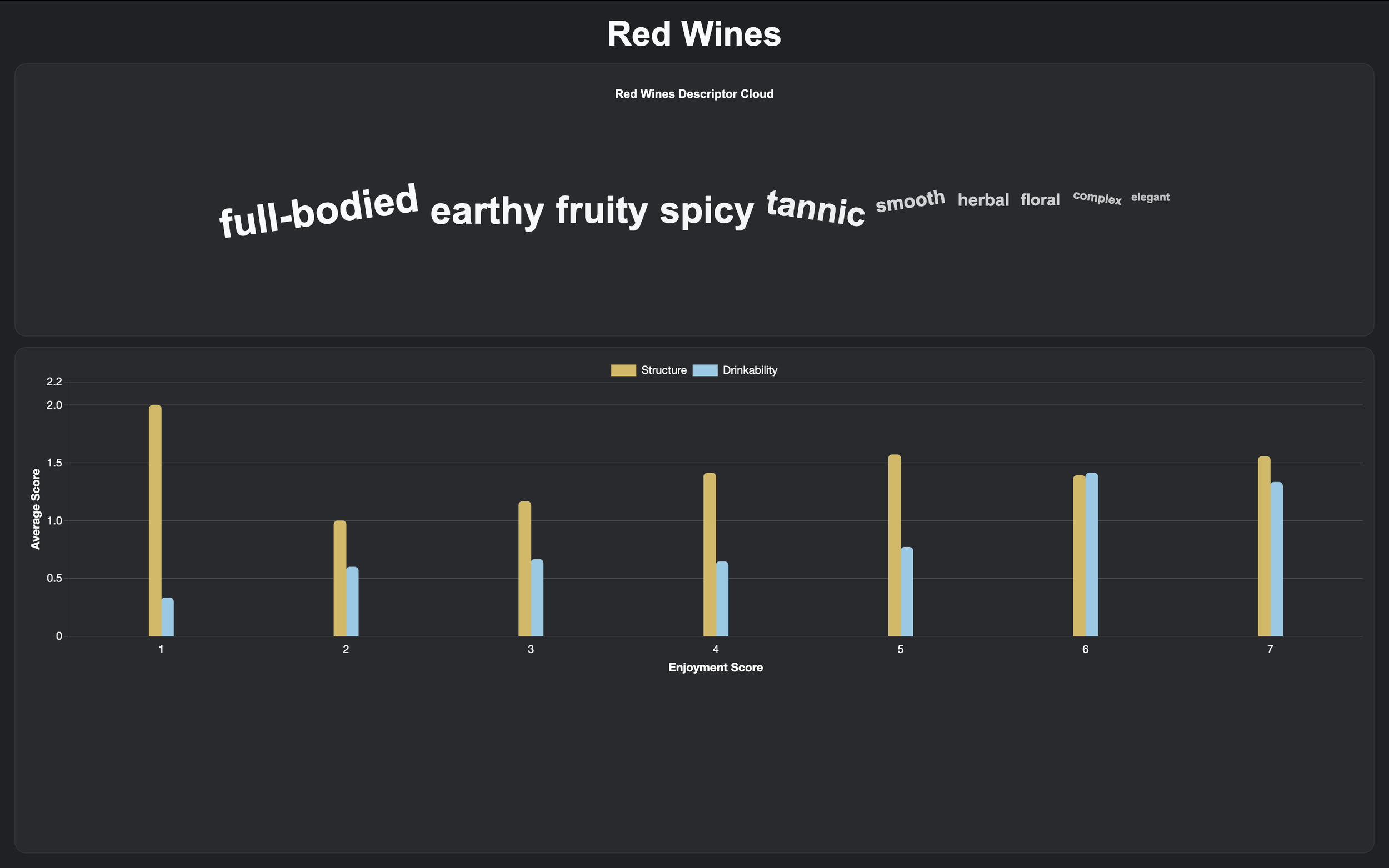

RED WINES

For reds, the top three regions by average enjoyment were Umbria (5.45), Sardegna (5.06), and Sicilia (5.00). Recognition also clustered around Umbria and Sardinia, suggesting a level of typicity that experienced tasters could pick up even blind.

When you look at descriptors, you see two layers of preference. The broader red vocabulary leaned toward “full-bodied,” “earthy,” “fruity,” “spicy,” “tannic.” People appreciate presence. But the very top wines tended to combine structure with a feeling of ease. The Structure vs Drinkability analysis makes that clear: lower-scoring reds were perceived as high-structure but low-drinkability; higher enjoyment scores came when the two moved closer together.

WHITE WINES

Whites were described with a consistent set of words “fresh,” “fruity,” “mineral,” “citrus,” “floral.” The top white wine was Falanghina del Sannio DOC, followed closely by Etna Bianco DOC and Trebbiano Spoletino.

That top three is telling: it mixes crowd-pleasing freshness with wines that carry clear place-driven personality (Etna’s volcanic profile, for example). The Structure vs Drinkability reading reinforces it: at enjoyment score 6, structure peaks, suggesting the highest-scoring whites were valued for being more than easy-drinking.

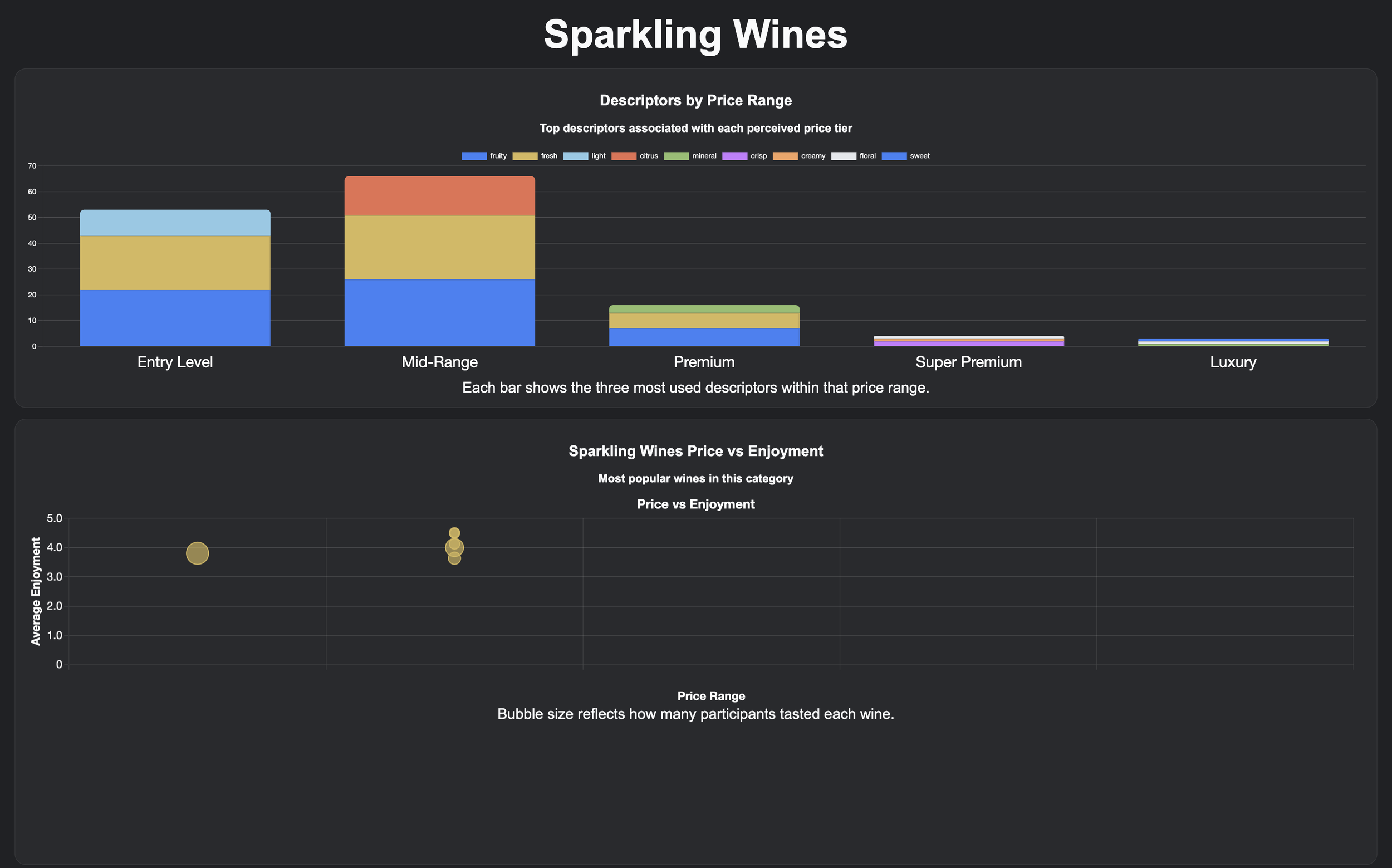

SPARKLING WINES

Sparkling descriptors clustered around “fruity,” “fresh,” “citrus,” “crisp,” with touches of “floral” and “mineral.” The standout sparkling was a Rosé Lambrusco di Modena DOC, both the most liked and the most recognised, with 63% correct identification. That “loved + recognised” combination is powerful commercially because it means that the wine communicates its identity quickly, even in a blind context.

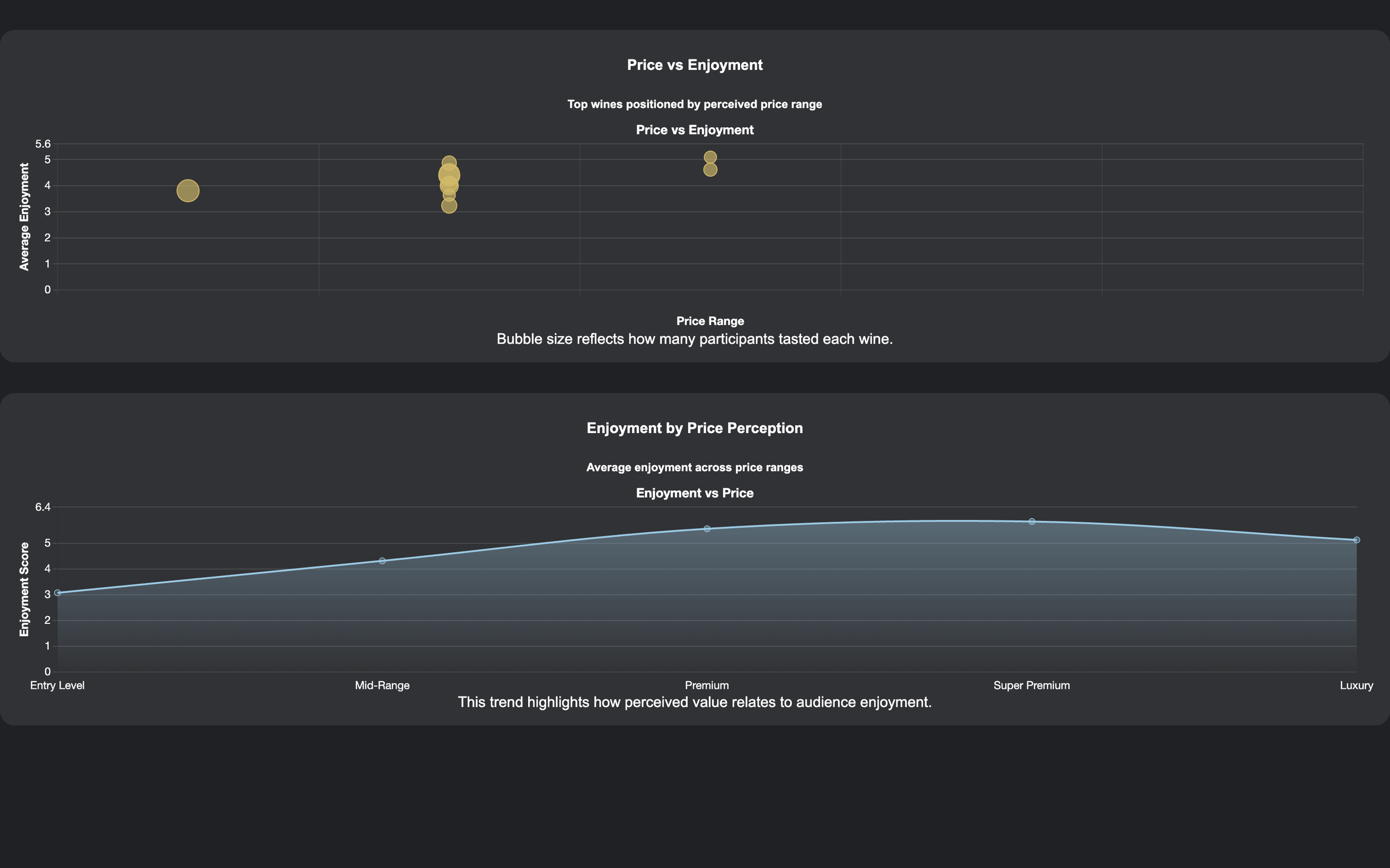

Perceived Value per Price Range

In the blind tasting, participants didn’t guess the exact retail price. They did something more interesting: they placed each wine into a perceived tier (Entry, Mid-Range, Premium, Super Premium, Luxury), then we mapped that perception against enjoyment. What came out is a pattern buyers see every day: enjoyment climbed steadily from Entry through Super Premium, then softened slightly at Luxury (with a smaller sample size there). In plain terms we can say that the wines that made people happiest were the ones that felt high-quality and layered, while still staying legible and comfortable. Super Premium becomes a kind of “confidence zone”: the point where the wine signals seriousness (complexity, structure, finesse) without feeling distant or overly formal. That’s also why this datapoint is commercially useful because it is not only about price but more about value cues. The audience rewarded wines that communicated quality in the glass, regardless of the real price behind them.

When we look at the descriptors people used inside each perceived tier, you can almost see the audience building a price ladder in real time.

Reds: At Entry and Mid-Range, red wines were described mainly as tannic, fruity, full-bodied. Those are the words of immediate impact: you taste it, you feel it, you can describe it quickly. As perceived price moved into Premium, language shifted toward earthy and herbal. That’s a subtle but meaningful change showing that the audience is picking up secondary complexity, not just fruit and structure. At Super Premium, herbal and floral became even more prominent and this is aligned with the classic “fine-wine” perception: aromatic lift and nuance start functioning as value signals. It’s less about weight, more about detail.

Whites: At Entry Level, whites were described with the “comfort vocabulary” people reach for when a wine feels immediately easy and pleasant words like fresh, fruity and citrus were the most used to describe this section. As perceived price moved into Mid-Range, the language gained definition, mineral and structured started showing up alongside freshness, which usually signals that tasters are sensing more than primary fruit: a little tension, a little backbone, something that holds the palate. At Premium, that combination became even clearer, mineral and structured stayed prominent while fresh remained present, suggesting that for this audience “premium white” is less about richness and more about precision. Super Premium and Luxury were more lightly sampled, but the descriptors leaned toward elegant and herbal, which, as we saw for the reds too, fits to a classic fine-white perception, a less overt sweetness of fruit, leaning instead to a more detail, restraint, and a longer, more composed finish.

Sparkling: Sparkling showed the strongest concentration in Entry and Mid-Range tiers, reflecting both what was poured and how people tend to anchor sparkling pricing. In Entry Level, the descriptors clustered around fruity, fresh, and light. In Mid-Range, citrus became more central while fresh stayed strong and fruity softened slightly, as if the audience was reading “brightness and precision” as a step up in quality. The Premium tier is where mineral language started to appear, which is a meaningful shift: when tasters describe sparkling as mineral, they’re often picking up structure and depth rather than simple aromatic charm.

What this blind tasting really gave us was a clean view of how taste turns into value when the usual shortcuts disappear. The wines that scored best weren’t necessarily the boldest or the best known; they were the ones that felt clear, balanced, and easy to understand on the palate. You see it in the language people used again and again, fresh, mineral, citrus, floral, elegant, and you see it in the way structure only becomes an advantage when it stays enjoyable, not heavy.

The pricing exercise adds a second layer that’s even more useful commercially. People didn’t reward “expensive.” They rewarded wines that feel serious while still feeling comfortable to drink. That Super Premium “confidence zone” is basically the sweet spot where quality is obvious, complexity is present, and the wine still feels approachable. Even more interesting, the descriptors show how that value is built: reds move from impact to nuance, whites move from comfort to precision, sparkling moves from simple refreshment to depth.

For producers and buyers, that’s the takeaway: today’s market appetite leans toward identity that’s legible, quality that shows up through detail, and balance that invites the next sip. The Data Hub is there to keep making those signals visible, so Italian native varieties can be positioned with more accuracy, and with language that matches how people actually respond when they taste.